Understanding how Bitcoin is taxed might not be the most exciting part of your crypto journey, but it's absolutely essential. Whether you're a casual holder who bought some satoshis years ago or an active trader moving in and out of positions, tax authorities around the world have increasingly clear expectations about how you report your cryptocurrency activities.

The challenge? Tax treatment varies dramatically depending on where you live. What's completely tax-free in one country could trigger significant capital gains obligations in another. Some nations embrace Bitcoin with favorable tax frameworks, while others treat every transaction as a taxable event.

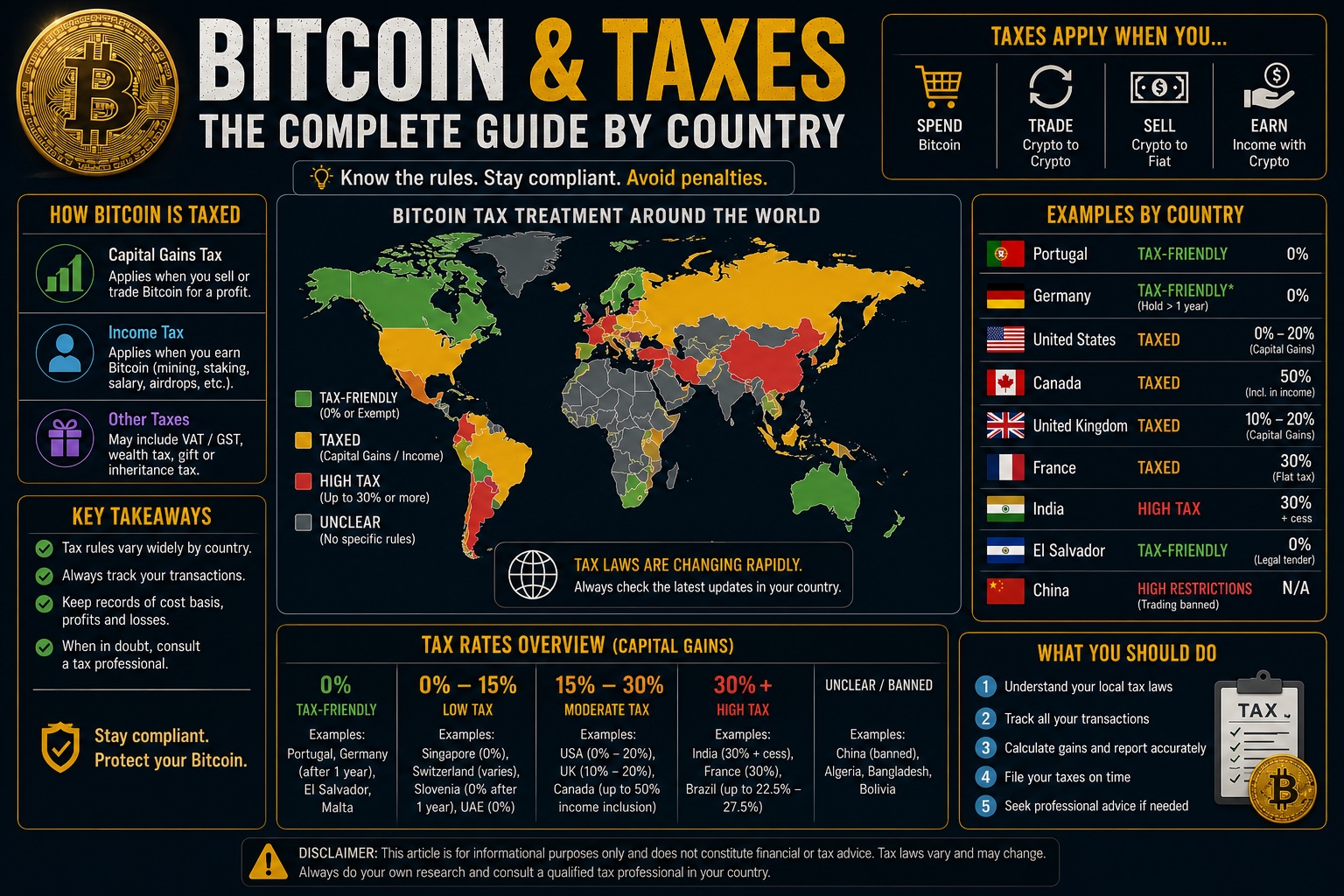

In this comprehensive guide, we'll walk through how major countries approach Bitcoin taxation, explain the common types of taxable events you need to track, and share practical strategies for staying compliant while minimizing your tax burden legally. Consider this your trusted roadmap to navigating the complex intersection of Bitcoin and taxes.

Understanding Bitcoin Taxable Events: The Basics

Before diving into country-specific rules, let's establish what typically triggers a tax obligation when dealing with Bitcoin. While specifics vary by jurisdiction, most tax authorities recognize similar types of taxable events.

Capital Gains and Losses

The most common taxable event occurs when you dispose of Bitcoin. This includes:

- Selling Bitcoin for fiat currency (USD, EUR, GBP, etc.)

- Trading Bitcoin for other cryptocurrencies (yes, swapping BTC for ETH is typically taxable)

- Using Bitcoin to purchase goods or services

- Gifting Bitcoin (in some jurisdictions)

Your capital gain or loss is calculated as the difference between your cost basis (what you paid for the Bitcoin, including fees) and the fair market value at the time of disposal.

Example: You purchased 0.5 BTC for $15,000 in 2022. Two years later, you sell it for $25,000. Your capital gain is $10,000, which may be subject to taxation depending on your country's rules.

Income from Bitcoin

Receiving Bitcoin as payment triggers income tax obligations in most countries:

- Mining rewards — taxed as income when received

- Staking rewards — typically treated as income

- Payment for goods or services — taxed at fair market value when received

- Airdrops and hard forks — often treated as income

The key distinction is that income is taxed when you receive Bitcoin, while capital gains are taxed when you dispose of it. This means you could face two tax events: once when you earn Bitcoin and again when you sell it.

Bitcoin Tax Treatment in the United States

The Internal Revenue Service (IRS) treats Bitcoin and other cryptocurrencies as property for tax purposes, not currency. This classification has significant implications for American taxpayers.

Capital Gains Tax Rates

The US distinguishes between short-term and long-term capital gains:

- Short-term gains (assets held less than one year): Taxed as ordinary income, with rates ranging from 10% to 37% based on your tax bracket

- Long-term gains (assets held more than one year): Preferential rates of 0%, 15%, or 20% depending on income level

This creates a strong incentive to hold Bitcoin for at least one year before selling, potentially saving significant money on taxes.

Reporting Requirements

US taxpayers must report all cryptocurrency transactions on their tax returns. The IRS asks directly on Form 1040 whether you've received, sold, exchanged, or otherwise disposed of any digital assets during the tax year.

For detailed reporting, you'll use:

- Form 8949 — to report each individual transaction

- Schedule D — to summarize your capital gains and losses

- Schedule 1 or Schedule C — for cryptocurrency income

Pro tip: Keep meticulous records of every transaction. When you purchase Bitcoin through exchanges like Binance, download your transaction history regularly. These records should include dates, amounts, fair market values, and any fees paid.

Bitcoin Taxation Across Europe

European countries have developed diverse approaches to cryptocurrency taxation, ranging from highly favorable to strictly regulated.

Germany: The HODL-Friendly Approach

Germany offers one of the most Bitcoin-friendly tax environments in Europe. If you hold Bitcoin for more than one year, any gains are completely tax-free, regardless of the amount. This applies to individuals, not businesses.

For holdings under one year, gains are taxed as private sales at your personal income tax rate (up to 45%). However, there's an annual exemption of €600 — if your total gains from private sales stay below this threshold, no tax is due.

United Kingdom: Capital Gains with Allowances

The UK treats Bitcoin as a capital asset. Key points include:

- Capital Gains Tax applies at 10% (basic rate) or 20% (higher rate)

- An annual tax-free allowance exists (though this amount changes periodically)

- Income received in Bitcoin is subject to Income Tax and potentially National Insurance

UK residents must keep detailed records for at least five years after the January 31 filing deadline.

Portugal: Shifting Landscape

Portugal was once famous for having zero taxes on cryptocurrency gains for individuals. However, this changed with new legislation introducing a 28% flat tax on crypto gains from assets held less than one year. Assets held longer than one year remain tax-free for individual investors, making Portugal still relatively attractive for long-term holders.

Switzerland: Canton-by-Canton Variations

Switzerland treats Bitcoin held as private assets as tax-free regarding capital gains. However, your Bitcoin holdings are subject to wealth tax, calculated annually based on your total net worth. Professional traders are subject to income tax on their gains. The exact rates depend on which canton you reside in.

Bitcoin Taxes in Asia-Pacific Region

The Asia-Pacific region presents a wide spectrum of regulatory approaches, from complete prohibition to tax-free havens.

Japan: Strict but Clear

Japan classifies cryptocurrency gains as miscellaneous income, which means they're taxed at progressive rates up to 55% (including local taxes). This is notably higher than the treatment of traditional investments. There's no distinction between short-term and long-term holdings, and trading between cryptocurrencies is a taxable event.

Australia: Comprehensive Framework

The Australian Taxation Office (ATO) has developed detailed guidance:

- Capital Gains Tax applies to disposal of Bitcoin

- A 50% CGT discount is available for assets held more than 12 months

- Personal use exemption exists for Bitcoin acquired and used to purchase goods or services (with limits)

- Mining and staking rewards are taxed as ordinary income

Australia requires particularly thorough record-keeping, including evidence of the date and time of transactions, amounts, and the purpose of the transaction.

Singapore: Tax-Free Capital Gains

Singapore does not impose capital gains tax, making it attractive for Bitcoin investors. However, businesses that deal in cryptocurrency may be subject to income tax on profits. Goods and Services Tax (GST) considerations may also apply to certain cryptocurrency transactions.

Tax Planning Strategies for Bitcoin Investors

Regardless of where you live, several legitimate strategies can help optimize your tax situation.

1. Utilize Long-Term Holding Periods

Many jurisdictions offer preferential treatment for long-term holdings. In the US, holding for over a year qualifies for lower capital gains rates. In Germany, holding for over a year makes gains completely tax-free. Plan your sales around these thresholds when possible.

2. Implement Tax-Loss Harvesting

If you have Bitcoin positions at a loss, you may be able to sell them to realize the loss and offset gains from other investments. Be aware of wash sale rules in your jurisdiction — some countries restrict immediately rebuying the same asset.

Example: You have $5,000 in gains from selling one Bitcoin position but hold another position with $3,000 in unrealized losses. By selling the losing position, you could reduce your taxable gains to $2,000.

3. Maintain Impeccable Records

Good record-keeping isn't just about compliance — it's about ensuring you can prove your cost basis accurately. Without records, tax authorities may assume a cost basis of zero, dramatically increasing your tax liability.

Store your Bitcoin securely on hardware wallets like Ledger devices, which also help you maintain clear records of your holdings and their acquisition dates. Having your private keys secured while maintaining transaction documentation serves both security and tax purposes.

4. Consider Cost Basis Methods

Different accounting methods can significantly impact your tax bill:

- FIFO (First In, First Out) — assumes you sell your oldest Bitcoin first

- LIFO (Last In, First Out) — assumes you sell your newest Bitcoin first

- Specific Identification — allows you to choose which specific units you're selling

Not all methods are available in all jurisdictions, and some countries mandate a specific approach. Consult a tax professional to determine the optimal strategy for your situation.

5. Track Every Transaction Automatically

Manual tracking becomes impractical quickly. Consider using cryptocurrency tax software that connects to exchanges like Binance and automatically imports your transaction history. These tools can calculate gains and losses, apply the appropriate accounting method, and generate tax reports compatible with your country's requirements.

Record-Keeping Best Practices

Proper documentation is your best defense in case of an audit and ensures accurate tax reporting. Here's what to track for every transaction:

- Date and time of the transaction

- Type of transaction (purchase, sale, trade, income)

- Amount of Bitcoin involved

- Fair market value in your local currency at the time

- Fees paid (which typically add to your cost basis)

- Running balance of your holdings

- Wallet addresses involved

- Purpose of the transaction

Store these records in multiple locations — both digital and physical backups if possible. Most tax authorities require you to keep records for several years after filing, but given Bitcoin's long-term potential, keeping records indefinitely is wise.

For security, use a hardware wallet like Ledger to store your Bitcoin safely while maintaining clear documentation of when each deposit was made. This creates a verifiable trail linking your exchange purchases to your secure storage.

Common Mistakes to Avoid

Even well-intentioned Bitcoin investors make tax errors. Here are the most frequent pitfalls:

- Thinking crypto-to-crypto trades aren't taxable — In most jurisdictions, trading Bitcoin for another cryptocurrency is a taxable disposal

- Forgetting about small transactions — Every purchase made with Bitcoin, even buying coffee, is typically a taxable event

- Ignoring airdrops and forks — Free tokens usually count as taxable income when received

- Not reporting because you didn't receive a tax form — The obligation to report exists whether or not you receive official forms

- Using incorrect cost basis — Losing track of what you paid leads to overpaying or underpaying taxes

- Missing DeFi transactions — Yield farming, liquidity provision, and other DeFi activities create taxable events

Frequently Asked Questions

Do I owe taxes if I just hold Bitcoin and never sell?

In most countries, simply holding Bitcoin does not create a taxable event. You typically only owe capital gains taxes when you sell, trade, or otherwise dispose of your Bitcoin. However, some countries like Switzerland impose a wealth tax on your total holdings, including Bitcoin. Additionally, any Bitcoin you receive as income (from mining, staking, or payment for services) is usually taxable when received, regardless of whether you sell it.

What happens if I don't report my Bitcoin on my taxes?

Failing to report cryptocurrency transactions can result in serious consequences including penalties, interest on unpaid taxes, and in severe cases, criminal prosecution for tax evasion. Tax authorities worldwide are becoming increasingly sophisticated at tracking cryptocurrency transactions through exchange data sharing agreements and blockchain analysis. Most major exchanges report user data to tax authorities in their jurisdictions. If you've failed to report in previous years, consider consulting a tax professional about voluntary disclosure programs that may reduce penalties.

How do I calculate taxes when I've bought Bitcoin at many different prices?

When you've accumulated Bitcoin through multiple purchases at varying prices, you need to track each purchase as a separate tax lot with its own cost basis. When you sell, you'll apply an accounting method (FIFO, LIFO, or specific identification where allowed) to determine which tax lots are being sold. For example, using FIFO, if you bought 0.1 BTC at $20,000 and later 0.1 BTC at $30,000, selling 0.1 BTC would use the $20,000 cost basis first. Crypto tax software can automate this calculation across hundreds or thousands of transactions.

Are there any countries where Bitcoin is completely tax-free?

Several jurisdictions offer very favorable tax treatment for Bitcoin investors. As of current regulations, long-term holders in Germany (over one year) and Portugal (over one year) pay no capital gains tax. Singapore and the UAE have no capital gains tax generally, which extends to cryptocurrency. However, tax laws change frequently, and other taxes like income tax or wealth tax may still apply. Always verify current regulations with a local tax professional before making decisions based on tax considerations.

Do I need to report Bitcoin I received as a gift?

Gift tax rules vary significantly by country. In the US, receiving a gift of Bitcoin isn't immediately taxable to you — your cost basis becomes the giver's original cost basis. However, the person giving the gift may need to file a gift tax return if the value exceeds annual exclusion limits. When you eventually sell the gifted Bitcoin, you'll owe capital gains based on the original cost basis. In other countries, gifts may be taxed at the time of transfer, or the recipient may inherit a fair market value cost basis. Consult local regulations for specifics.

Conclusion

Bitcoin taxation is complex, varies dramatically by jurisdiction, and continues to evolve as governments refine their approaches to cryptocurrency. The key takeaways for any Bitcoin investor are clear: understand your local tax obligations, keep meticulous records of every transaction, and consider long-term holding strategies where beneficial.

While this guide provides a comprehensive overview, tax situations are individual. The interaction between your specific circumstances — residency, trading frequency, other income, and more — makes professional advice invaluable for significant holdings or complex situations.

Stay proactive about compliance. The cryptocurrency industry's maturation means increased regulatory scrutiny and improved government tracking capabilities. The cost of getting it right from the start is far lower than dealing with audits, penalties, and interest down the road.

Whether you're just getting started buying Bitcoin on exchanges like Binance or you're a seasoned holder securing your stack on a Ledger hardware wallet, integrating tax awareness into your Bitcoin strategy isn't optional — it's essential for sustainable, long-term success in this asset class.